10/17/2024

10/17/2024

Most businesses look responsible on the surface. Underneath, informal safeguards are doing the actual work.

You have insurance. Contracts get reviewed occasionally. Cash balances stay monitored. That is not risk management. That is risk absorption, and the difference is not semantic. Risk absorption is what happens when exposure accumulates through informal controls, unclear decision authority, and inconsistent governance while the organization believes it is protected. The layered ambiguity builds quietly. The exposure becomes expensive suddenly.

This article names what risk absorption actually looks like in operational practice, what governance frameworks address it structurally, and why daily integration beats quarterly review every time.

In This Article

- Risk Absorption Starts With Informal Controls

- Risk Absorption Is Layered Ambiguity

- Unclear Decision Rights Multiply Risk

- Governance Frameworks Reduce Risk Absorption

- Documentation Inconsistency Creates Exposure

- Risk Management Requires Daily Integration

- How GetSysPro Addresses Risk Absorption

- Frequently Asked Questions

Key Takeaways

- Risk absorption is not a dramatic event. It is layered operational ambiguity that accumulates through informal controls, unclear authority, and inconsistent governance until exposure becomes expensive.

- Insurance and occasional contract review are not risk management. Risk management requires documented controls, defined decision rights, and consistent review cadence integrated into daily operations.

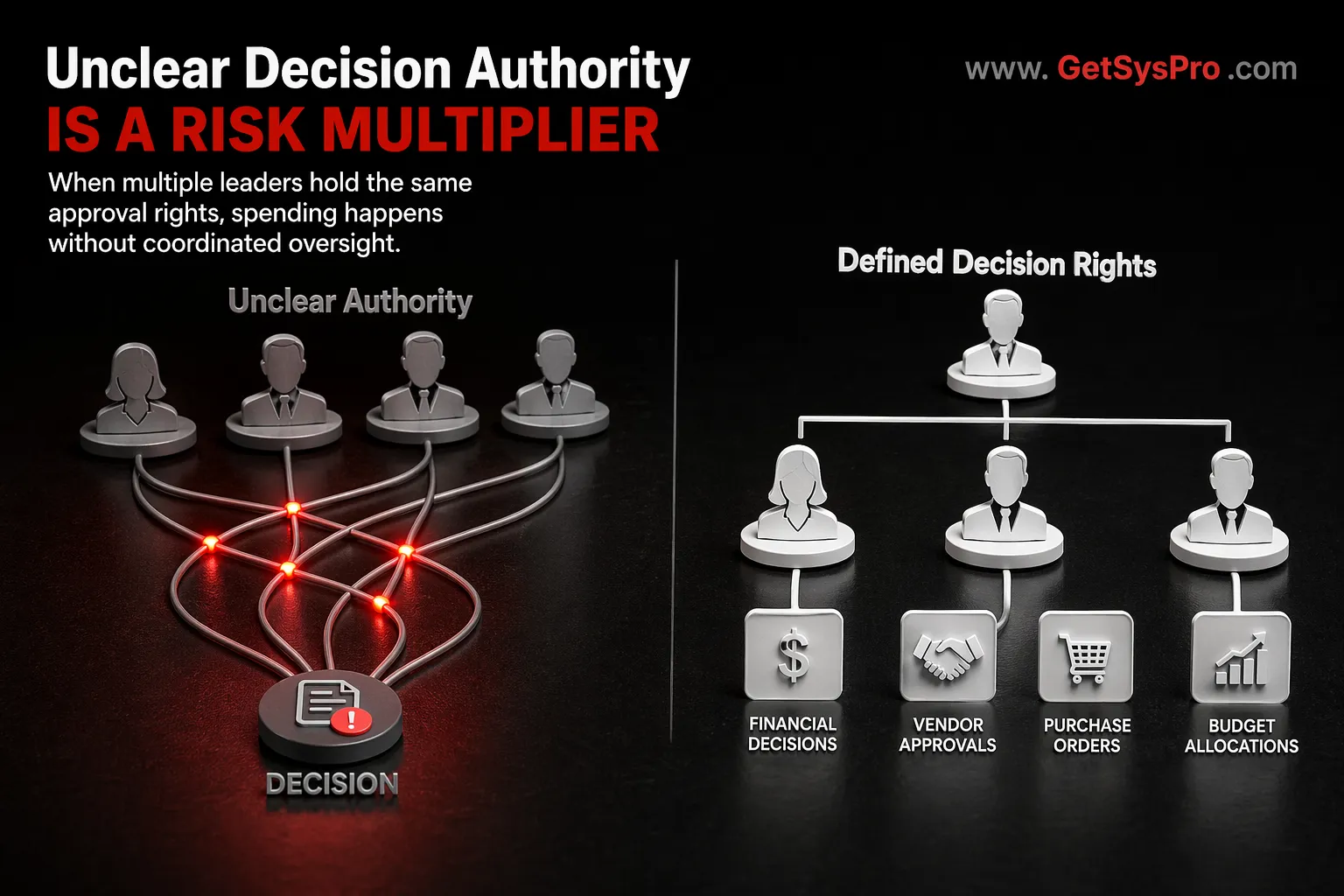

- Unclear decision authority is one of the most overlooked risk multipliers. When multiple leaders believe they hold approval rights, spending and commitments lack coordinated oversight and financial exposure increases.

- Documentation inconsistency creates legal and operational ambiguity. Vague contract clauses, outdated templates, and informal vendor terms weaken enforcement and increase dispute exposure.

- Governance does not eliminate risk. It distributes and contains it, converting uncertainty into monitored variables rather than unexpected shocks.

Risk Absorption Starts With Informal Controls

Risk absorption happens when safeguards are optional, inconsistent, or exist only in someone’s memory. Vendor agreements vary by relationship rather than by documented standard. Approval thresholds live in a manager’s head rather than in a written policy. Reporting cadence is irregular because nobody owns it. Roles overlap without documented authority boundaries because the org chart was never updated after the last hiring wave. None of those gaps looks catastrophic in isolation. The exposure they create compounds quietly until something triggers it.

The ACFE’s Occupational Fraud 2024 findings identify a lack of internal controls as among the most commonly cited organizational weaknesses in fraud cases, with many instances involving either missing controls entirely or the override of controls that nominally existed. Fraud is one dimension. The broader principle applies across every category of operational risk: informal systems invite loss because they create the gaps that losses pass through.

What Informal Controls Actually Look Like

Informal controls do not look like negligence. They look like normal operations in a fast-moving organization. A vendor gets onboarded without a standard agreement because the relationship is trusted and urgent. Spending gets approved verbally because writing it up takes time nobody has right now. Compliance deadlines get tracked in someone’s calendar rather than a shared system because it has always worked that way. Each of those decisions is defensible individually. Collectively they describe an organization managing risk by absorbing it rather than by controlling it.

“Governance does not eliminate risk. It distributes and contains it. The goal is not zero exposure. The goal is transforming uncertainty into monitored variables rather than unexpected shocks that arrive without warning and cost more than they should.”

Editorial, GetSysPro Team

Risk Absorption Is Layered Ambiguity

Risk absorption rarely feels like taking on risk. It feels like getting things done. A contract clause gets left vague because the other party is trusted and the negotiation would be uncomfortable. Vendor relationships go unreviewed because delivery has always been fine. Capital expenditures get approved without documentation because the need is urgent and the paperwork will come later. Compliance deadlines get assumed rather than tracked because nobody wants to be the person who slows things down to set up a formal system.

Each of those exceptions seems manageable in the moment. Collectively they describe an organization that reacts to risk rather than prevents it, absorbing exposure through the cumulative effect of reasonable-sounding deferrals that nobody intended to leave in place permanently.

Why Layered Ambiguity Is Harder to See Than Single Failures

Single failures are visible and prompt responses. Layered ambiguity is invisible because no single element is alarming enough to trigger action on its own. The vague contract clause sits in a file. An unreviewed vendor relationship continues delivering. The undocumented approval gets filed. That assumed deadline passes, this time. The exposure exists in the aggregate, not in any individual item. Risk absorption compounds through that invisibility until something in the aggregate fails, at which point the full cost of the deferred structural work arrives simultaneously and without warning.

Unclear Decision Rights Multiply Risk

One of the most overlooked risk multipliers in growing organizations is informal decision authority. When multiple leaders believe they hold approval rights for the same category of decision, inconsistency becomes the operating norm. Two different managers approve two different vendors for the same service at two different prices under two different terms. Three people commit the organization to three overlapping obligations because nobody knew the others were in parallel conversations. Accountability blurs because the boundaries between who decides what were never drawn.

Financial exposure increases directly from that ambiguity. Spending and commitments made without coordinated oversight exceed planned budgets. Contractual obligations get assumed without senior review. Vendor relationships get structured by whoever happens to be managing them at the time rather than by consistent organizational standards. Control is not created by good intentions. It is created by decision rights that are documented, understood, and enforced consistently across every level that touches financial and operational commitments.

The Connection Between Decision Rights and Risk Absorption

The connection between undefined decision rights and risk absorption is direct. Every decision made outside a defined authority structure is a decision made without the oversight that authority structures exist to provide. Some of those decisions will be correct. Others will create exposure that the organization discovers later, during a vendor dispute, an audit, a contract renewal negotiation, or a leadership transition. Defined decision rights do not slow organizations down. They prevent the category of risk that accumulates through well-intentioned decisions made by the wrong people or without the context that coordinated oversight provides.

Governance Frameworks Reduce Risk Absorption

Governance is not bureaucracy. It is operational insurance that reduces variability and limits surprise. Organizations that treat governance as an administrative burden they will get to eventually are making a specific trade: they are exchanging the cost of building controls now for the higher cost of absorbing the losses those controls would have prevented.

The COSO internal control framework organizes governance into five components: control environment, risk assessment, control activities, information and communication, and monitoring. COSO’s framework for internal controls provides a structured approach for building the oversight architecture that converts informal safeguards into documented, enforceable controls across the organization.

What Governance Actually Changes in Daily Operations

Governance changes the organizational default from reactive to preventive. Without governance, the default is to proceed until something goes wrong and then respond. With governance, the default is to maintain the control environment that makes going wrong less likely and detectable sooner when it does happen. That shift does not require an enterprise risk management program or a compliance department. It requires documented controls for the decisions and processes that carry the most exposure, consistent enforcement of those controls, and a review cadence that surfaces variance before it compounds into loss.

Documentation Inconsistency Creates Exposure

Copy-paste contracts, outdated templates, informal partnership terms, and nonstandard vendor clauses create legal and operational ambiguity that most organizations do not recognize as risk until something triggers a dispute. Ambiguous language weakens enforcement because both parties can reasonably interpret the same clause in their favor. Outdated templates contain terms that no longer reflect the organization’s current operational reality or legal environment. Informal terms create obligations that were never formally reviewed and may not be enforceable or may be enforceable in ways the organization did not intend.

Precision in documentation creates precision in execution. When contracts reflect current operational standards, when vendor agreements define expectations for pricing, scope, response time, and dispute resolution, and when internal documents use consistent terminology for the same concepts, the organization reduces the ambiguity through which disputes, losses, and unexpected obligations enter.

Documentation as a Risk Control, Not an Administrative Task

Organizations that treat documentation as administrative overhead consistently underinvest in it relative to its risk reduction value. A contract clause that takes thirty minutes to write precisely can prevent a dispute that takes months to resolve expensively. A vendor agreement template that reflects current standards reduces the variation that produces inconsistent vendor relationships across the organization. Documentation is not the end product of operational discipline. It is the mechanism through which operational discipline becomes enforceable and consistent rather than dependent on individual memory and good intentions.

Are informal controls doing the actual risk work in your business?

GetSysPro audits where risk absorption has accumulated and builds the governance structure that converts exposure into controlled, monitored variables.

Risk Management Requires Daily Integration

Risk management fails when it lives in quarterly discussions rather than daily operating design. A quarterly risk review is better than nothing. It is not a substitute for controls embedded in the processes where risk actually originates. By the time a quarterly review surfaces an exposure, that exposure has typically been accumulating for weeks or months and has already produced consequences that earlier detection would have prevented or reduced.

ISO 31000 emphasizes that risk management should be supported by a framework and carried out through a process that includes risk identification, analysis, evaluation, and treatment with ongoing monitoring rather than periodic review. ISO 31000’s approach to risk management frames risk management as an integrated organizational discipline rather than a compliance exercise, which is the distinction between organizations that absorb risk and those that manage it.

What Daily Integration Actually Looks Like

Daily integration means that controls, approvals, and reporting are embedded in the workflows where decisions and commitments occur, not reviewed separately after those decisions are already made. Vendor approvals happen through a defined process before commitments are made, not audited after the fact. Financial variance gets reviewed on a cadence that surfaces problems before they compound, not at quarter end when the variance is already historical. Compliance deadlines appear in shared systems with assigned owners, not in individual calendars where their status is invisible to anyone else. That integration converts risk absorption into risk management by closing the gaps between when exposure originates and when oversight reaches it.

How GetSysPro Addresses Risk Absorption

Risk absorption accumulates through process gaps rather than through revenue collapse: unclear approvals, inconsistent vendor payment cycles, reactive forecasting, and irregular variance review. Connecting financial and operational performance to the workflows and decision paths that create or reduce exposure is where structural risk reduction begins.

GetSysPro Services That Reduce Risk Absorption

A Business Operational Systems Audit identifies where risk absorption has accumulated: the approval gaps, reporting inconsistencies, unclear decision rights, and accountability ambiguities that convert operational informality into organizational exposure.

Specialized Documents Creation strengthens structural discipline by aligning contracts, vendor agreements, and internal documents with current operational reality so that documentation precision converts into execution precision rather than leaving ambiguity where disputes enter.

Related GetSysPro Services

When multiple leaders believe they hold the same approval rights, spending and commitments happen without coordinated oversight. Defined decision rights close that gap. www.GetSysPro.com

Article Summary

Risk absorption is not dramatic. It is layered operational ambiguity that accumulates through informal controls, unclear decision authority, and inconsistent governance. Insurance and occasional contract review are surface-level protection, not structural risk management. Unclear decision rights multiply exposure by creating spending and commitments without coordinated oversight. Documentation inconsistency generates legal and operational ambiguity through which disputes and unexpected obligations enter. Governance frameworks convert informal safeguards into documented, enforceable controls. Daily integration embeds risk management in the workflows where exposure originates rather than reviewing it quarterly after the damage is already done. GetSysPro audits where risk absorption has accumulated and builds the structural controls that convert uncertainty into monitored variables.

Stop Absorbing Risk. Start Managing It.

GetSysPro builds the governance structure, decision rights, and documentation discipline that convert informal safeguards into structural risk controls.

Frequently Asked Questions

What is the difference between risk management and risk absorption?

Risk management means controls, decision rights, and oversight are documented, enforced, and embedded in daily operations so that exposure is identified before it compounds. Risk absorption means the organization proceeds under informal safeguards that leave gaps through which exposure accumulates. The practical difference is whether risk is actively governed or passively carried through the absence of structural controls.

Why do informal controls feel adequate until they are not?

Informal controls feel adequate because they work most of the time. Trusted vendors deliver. Verbal approvals produce correct decisions. When they do fail, however, the failure is not contained by structural safeguards. A single vendor dispute or missed compliance deadline can cost more than building formal controls would have across several years.

How do unclear decision rights create financial exposure?

When multiple leaders believe they hold approval authority for the same decision category, spending and commitments happen without coordinated oversight. Two managers approve overlapping vendor contracts. Budget assumptions get bypassed because nobody is certain who can authorize an exception. Defined decision rights prevent each instance by routing decisions through the oversight the expenditure or commitment requires.

What makes documentation a risk control rather than just an administrative task?

Documentation is a risk control because it defines the terms under which obligations are enforced. Vague contract language creates ambiguity both parties can interpret in their favor during a dispute. Outdated vendor templates no longer reflect current operational standards. Informal partnership terms create obligations enforceable in ways the organization never intended. Precise documentation closes those gaps with a shared, enforceable definition of expectations.

What does daily integration of risk management look like in practice?

Daily integration means controls and approval workflows are embedded in the processes where decisions originate, not applied afterward as an audit layer. Vendor approvals occur through a defined process before commitments are made. Financial variance gets reviewed on a cadence that surfaces problems before they compound. Compliance deadlines appear in shared tracking systems with assigned owners. Each mechanism closes the gap between when exposure originates and when oversight reaches it.