07/24/2024

07/24/2024

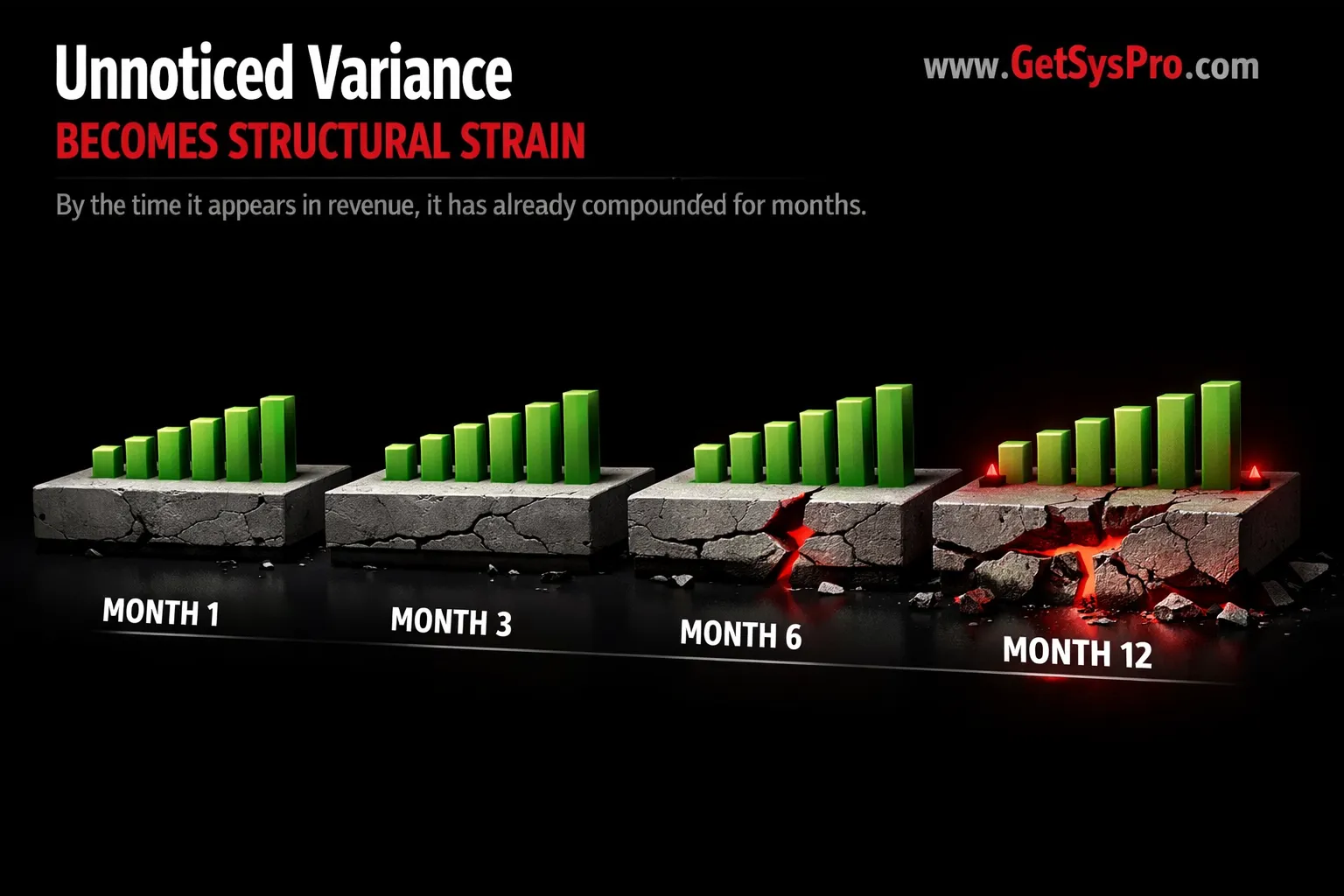

Financial blind spots rarely appear dramatic at first. They develop quietly inside growing organizations that rely on surface-level reporting instead of structural visibility, and by the time they surface in financial statements, they have already compounded for months.

Most business owners believe they understand their numbers. Monthly revenue is known. Payroll costs are roughly understood. Cash in the account feels comfortable. Comfort, however, is not control. Revenue can rise while margin quietly compresses. Payroll can increase without corresponding productivity gains. Vendor expenses can creep upward without renegotiation. Marketing spend can expand without measurable return. None of those variables trigger immediate alarm when leadership reviews only top-line summaries, which means financial blind spots accumulate precisely in the space between what is measured and what actually drives financial performance.

This article identifies the three financial blind spots that compound fastest in growing businesses, explains how financial clarity connects to operational performance, and outlines what structural visibility actually requires to protect a business that surface-level reporting is quietly exposing.

In This Article

- The Three Financial Blind Spots That Compound Fastest

- How Margin Erosion Hides in Plain Sight

- Financial Clarity Is Operational Clarity

- Informal Approval Culture Is a Quiet Financial Leak

- Why Growth Increases Financial Exposure

- What Financial Discipline Actually Looks Like

- How GetSysPro Addresses Financial Blind Spots

- Frequently Asked Questions

Key Takeaways

- Financial blind spots develop in the space between what is measured and what actually drives financial performance. Comfort with top-line numbers is not the same as structural financial visibility.

- The three financial blind spots that compound fastest are inconsistent reporting cadence, unclear cost attribution, and weak forecasting discipline. Each one allows trends to hide until they become expensive to reverse.

- Gross margin can slip a few points unnoticed and represent tens of thousands of dollars lost over twelve months through inefficiency rather than market pressure.

- Financial clarity is operational clarity. Numbers without operational context become historical reporting. Visibility becomes management only when it drives decisions.

- Financial problems rarely begin with crisis. They begin with unnoticed variance. Unnoticed variance becomes trend. Trend becomes strain. Structural visibility interrupts that sequence before the compounding makes it expensive.

The Three Financial Blind Spots That Compound Fastest

Financial blind spots typically emerge in three areas, each of which shares a common characteristic: the problem is invisible when examined at the level most leaders examine their finances, and visible only when reporting is structured to capture the detail that surface summaries omit. Understanding where financial blind spots live is the prerequisite to building the reporting infrastructure that eliminates them.

The first financial blind spot is inconsistent reporting cadence. Financial statements reviewed irregularly, or reviewed without variance analysis against a prior period or a forecast, allow trends to hide in plain sight. A cost category that increases by eight percent in one month looks unremarkable in isolation. Tracked against the prior three months with variance analysis, it reveals a pattern that signals a structural problem rather than a one-time fluctuation. Inconsistent cadence removes the pattern recognition that financial management requires.

Cost Attribution and Forecasting as Compounding Blind Spots

The second financial blind spot is unclear cost attribution. When expenses are not mapped accurately to departments, service lines, or projects, margin distortion occurs at a level the top-line summary never captures. Leaders optimize the wrong service lines, cut costs in areas that are not the source of margin pressure, and preserve spending in areas that are eroding profitability invisibly. Cost attribution clarity is not an accounting exercise. It is a management tool that connects financial performance to operational decisions.

The third financial blind spot is weak forecasting discipline. Without rolling projections that extend ninety days forward, leadership manages by bank balance rather than by anticipated trajectory. A comfortable bank balance today does not indicate financial health in ninety days when committed expenses, seasonal variation, payroll cycles, and planned investments are accounted for. Reactive financial management produces reactive cuts, delayed investments, and compounding stress even when the business is fundamentally healthy. Rolling forecasts replace reactive balance management with deliberate liquidity oversight that surfaces cash stress weeks before it arrives rather than days after.

“Financial blind spots are not a sign that a business is poorly managed. They are a sign that the reporting infrastructure has not scaled with the business complexity. Every stage of growth adds new sources of financial exposure. The reporting framework must evolve at the same pace or visibility declines precisely when the stakes are highest.”

Editorial, GetSysPro Team

How Margin Erosion Hides in Plain Sight

Gross margin erosion is one of the most common and most expensive financial blind spots in growing businesses because it is invisible at the revenue line. A business generating strong revenue growth looks healthy at the top of the income statement while losing ground at the margin line that determines whether that revenue actually builds financial strength or simply funds increasing costs.

The mechanism is straightforward. A few points of gross margin lost through rework, scope drift, vendor cost increases, or inefficient delivery processes may represent less than one percent of revenue in any given month. Over twelve months, that erosion can represent tens of thousands of dollars in profit that existed in the model but never materialized in performance. The compounding effect is what makes margin erosion a financial blind spot rather than a visible problem: each individual period looks close enough to acceptable that no alarm activates, and the cumulative damage only becomes visible in a detailed margin analysis that most businesses do not conduct regularly.

What Regular Variance Analysis Reveals That Monthly Totals Conceal

Monthly totals confirm that revenue arrived and expenses were paid. Variance analysis reveals whether the relationship between revenue and costs is improving, stable, or deteriorating and whether that trajectory reflects operational decisions the business is making or market forces it cannot control. A business that consistently tracks margin variance at the service line or project level develops early warning signals for cost creep before it becomes structural. One that reviews only monthly totals discovers margin erosion in the same review that reveals it has already compounded into a problem requiring a response rather than a prevention.

Financial Clarity Is Operational Clarity

Financial visibility is not only about accounting accuracy. Accounting accuracy ensures the numbers are correct. Financial visibility ensures those correct numbers connect to the operational decisions that produced them. Numbers without operational context are historical reporting. They tell you what happened without telling you why it happened or what operational change will produce a different outcome next period.

The connection between financial performance and operational behavior is where financial clarity becomes management rather than measurement. Aligning billing cycles with delivery milestones stabilizes revenue timing and makes cash flow more predictable. Vendor contracts reviewed on a defined cadence improve cost control because renegotiation happens before automatic renewals lock in pricing that no longer reflects market rates or actual usage. Department-level accountability connecting budget performance to operational behavior lets leaders identify the specific decisions and workflow patterns that drive financial outcomes rather than reacting to financial results without understanding their operational cause.

Why Reviewing Numbers Is Not the Same as Financial Management

Reviewing the numbers is a necessary step in financial management. It is not financial management itself. Financial management requires that the review produce decisions: to adjust a pricing structure, reallocate a budget, renegotiate a vendor contract, change a delivery process, or revise a forecast based on what actual performance reveals. Organizations that review financial reports without a structured framework for connecting those reports to operational decisions complete a ritual without extracting the management value the ritual is designed to produce. Financial blind spots persist in organizations that review their numbers regularly precisely because reviewing is not the same as managing.

Informal Approval Culture Is a Quiet Financial Leak

One of the most overlooked financial blind spots in growing organizations is informal approval culture. When expense approvals lack documented thresholds, consistent routing, and a clear record of what was approved, cost discipline weakens without any single decision appearing problematic. Small discretionary spending normalizes. Vendors add line items to invoices that nobody reviews carefully because the approval process does not require detailed validation. Tools and subscriptions renew automatically without an annual review that assesses whether they still deliver value proportional to their cost.

Each of those leaks is individually small. The aggregate is what creates the “mysterious” margin pressure that appears in financial reviews months after the leak began. The word mysterious reflects the absence of attribution, not the absence of a cause. Every dollar of unexplained margin compression has a cause. Informal approval culture removes the documentation trail that would make the cause identifiable and the leak fixable.

Building Approval Discipline Without Building Bureaucracy

Approval discipline does not require a bureaucratic approval process that slows every spending decision to a crawl. It requires three structural elements: defined thresholds that specify what requires approval and what does not, documented routing that ensures approvals reach the person with the information to evaluate them, and consistent recording that creates the audit trail that makes variance analysis possible. Those three elements allow the organization to move at appropriate speed while maintaining the cost visibility that prevents financial blind spots from forming in the approval process. Clarity and consistency achieve what rigidity cannot: cost discipline that scales with the business rather than constraining it.

Are financial blind spots quietly compressing your margins?

GetSysPro builds the operational and financial visibility infrastructure that surfaces blind spots before they compound into structural problems.

Why Growth Increases Financial Exposure

Financial blind spots are especially dangerous during growth cycles because growth multiplies the sources of financial exposure without automatically improving the reporting infrastructure that would surface them. Vendors add to the cost base. Service lines add margin complexity. Additional hires expand the payroll structure, and new tools accumulate subscription expense. Each addition is individually justifiable and collectively increases the financial surface area that reporting must cover to maintain visibility.

If the reporting framework does not evolve at the same pace as the business complexity it is designed to cover, visibility declines during the growth period that creates the most financial exposure. A reporting framework adequate for a five-person business at two million in revenue may miss significant financial blind spots in a fifteen-person business at five million in revenue, not because the quality of the reporting declined but because the complexity of the business outpaced the scope of the reporting. Growth does not create financial certainty. Without structural visibility investment, it creates financial exposure.

How Reporting Infrastructure Must Scale With Business Complexity

Scaling reporting infrastructure means adding cost attribution detail as new departments or service lines emerge, extending the forecasting horizon as cash flow complexity increases, building department-level budget accountability as headcount grows, and establishing vendor review cadences as the vendor base expands. None of those additions requires significant accounting investment. Each requires deliberate structural design of the reporting framework to ensure the questions that new complexity creates have corresponding answers in the financial visibility system. Organizations that treat reporting infrastructure as a static system in a growing business create financial blind spots not through negligence but through a failure to recognize that the system must scale with the complexity it monitors.

What Financial Discipline Actually Looks Like

Financial discipline in a growing business is not complexity. It is consistency applied to a small number of high-leverage practices that, together, eliminate the conditions under which financial blind spots develop and compound. Four practices account for the majority of the financial visibility that growing businesses need to protect performance.

Consistent performance review means financial statements examined on a fixed cadence, not when time permits. Monthly review is the minimum for most growing businesses. High-growth organizations benefit from weekly cash flow review in addition to monthly financial reporting. The cadence matters because financial trends require multiple data points to become visible, and irregular review delays the pattern recognition that early intervention requires.

Variance Analysis, Rolling Forecasts, and Budget Alignment

Monthly variance analysis compares actual performance against forecast and prior period at a level of detail sufficient to identify the operational cause of material variances. Total revenue and total expenses are not sufficient detail. Service line margin, department cost versus budget, and project-level profitability are the levels at which financial blind spots most frequently hide. Rolling cash flow forecasts extended ninety days forward replace reactive balance management with deliberate liquidity oversight. Departmental budgets aligned with measurable operational goals connect financial accountability to the behavior that produces it, so the people making decisions that drive financial outcomes have the visibility to understand the consequences before they make them. The AICPA’s guidance on cash flow management for growing businesses reinforces that forward-looking financial discipline consistently outperforms reactive monitoring in protecting business performance.

How GetSysPro Addresses Financial Blind Spots

Financial blind spots typically live at the intersection of process and finance. Rework creates cost without creating revenue. Decision latency delays billing and increases carrying cost. Unclear approval structures allow cost creep that no single decision produces but many small decisions accumulate. Inconsistent scope control erodes project margin that the revenue line never captures. A structured operational review identifies where those intersections are generating financial exposure before the financial statements confirm the damage.

GetSysPro Services That Build Financial and Operational Visibility

GetSysPro Business Operational Systems Audit connects financial performance to operational behavior by identifying where costs are rising, which processes create repeat errors that drive rework expenses, and where execution delays are pushing revenue recognition out while costs continue to accumulate. The goal is not to review numbers in isolation. It is to connect financial performance to how work actually moves through the business.

GetSysPro Process and SOP Architecture addresses the operational sources of financial blind spots by documenting workflows, defining approval thresholds, and standardizing delivery so execution quality is consistent rather than variable and its financial consequences are predictable rather than mysterious.

For organizations where financial blind spots connect to unclear departmental accountability and undefined decision rights, GetSysPro Organizational Chart Development defines the reporting relationships and accountability structures that connect financial performance to the specific roles responsible for producing it.

Related GetSysPro Services

Monthly totals look fine. Underneath, variance is compounding. Financial blind spots become structural strain before they ever appear in revenue. www.GetSysPro.com

Article Summary

Financial blind spots develop in the gap between what is measured and what actually drives performance. The three that compound fastest are inconsistent reporting cadence, unclear cost attribution, and weak forecasting discipline. Gross margin can erode a few points unnoticed and represent tens of thousands of dollars over twelve months. Financial clarity requires operational context, not just accounting accuracy. Informal approval culture creates the quiet leaks that produce mysterious margin pressure. Growth multiplies financial exposure without improving visibility unless the reporting framework scales deliberately. Financial discipline means consistent review, variance analysis, rolling forecasts, and budget accountability. GetSysPro builds the operational and financial visibility infrastructure that surfaces blind spots before they compound.

Visibility Is Discipline. Discipline Protects Performance.

GetSysPro builds the operational and financial visibility infrastructure that eliminates financial blind spots before they compound into structural problems your business cannot easily reverse.

Frequently Asked Questions

What are the most common financial blind spots in small and mid-sized growing businesses?

The three most common are inconsistent reporting cadence, unclear cost attribution, and weak forecasting discipline. Inconsistent cadence allows financial trends to hide in isolated period reviews that do not connect to a pattern. Unclear cost attribution creates margin distortion at the service line or project level that top-line summaries never surface. Weak forecasting discipline produces reactive cash management that generates stress and poor decisions even in fundamentally healthy businesses. Beyond those three, informal approval culture and the failure to scale reporting infrastructure alongside business complexity account for most of the financial blind spots that grow into structural problems in expanding organizations.

How can gross margin erode without appearing in monthly financial reviews?

Gross margin erosion hides in monthly reviews because monthly totals confirm revenue and expenses without revealing the relationship between them at the level where erosion actually occurs. A few points of margin lost through rework, scope drift, or vendor cost increases may appear as a small absolute variance that falls within a range leadership considers acceptable. Tracked across three to six months with consistent variance analysis at the service line or project level, the same data reveals a deteriorating trend that signals a structural problem. Monthly totals are necessary but not sufficient. Variance analysis against a forecast and a prior period at a meaningful level of cost detail is what makes margin erosion visible before it compounds.

What is the difference between reviewing financial reports and financial management?

Reviewing financial reports confirms that the numbers are available and that leadership has seen them. Financial management requires that the review produce decisions connected to the operational behavior that generated the numbers. A cost category increasing above forecast should produce an investigation into the operational cause and a decision about whether to address it. A margin variance should connect to a specific delivery process, vendor contract, or pricing decision that explains it. Financial management is the loop between financial data and operational decisions. Organizations that complete the reporting cycle without completing the decision cycle accumulate financial blind spots even in the presence of regular financial review.

How does informal approval culture create financial blind spots?

Informal approval culture removes the documentation trail that makes cost attribution possible and variance analysis meaningful. When expenses are approved informally, without documented thresholds or consistent routing, the approval record does not exist to connect the expense to the decision that authorized it. Small discretionary spending normalizes across many individuals and accumulates into material cost variance without any single decision appearing problematic. The “mysterious” margin pressure that appears in financial reviews several months after informal approval culture develops is not mysterious in cause. It is mysterious in attribution because the documentation that would identify the cause was never created. Defined thresholds, documented routing, and consistent recording are the three structural elements that close this financial blind spot.

At what growth stage should a business formalize its financial visibility infrastructure?

The practical answer is before complexity makes informality expensive rather than after it already has. For most businesses, the inflection point occurs somewhere between five and fifteen employees or between one and three million in annual revenue, when cost categories multiply, service lines or projects run simultaneously, and the founder’s direct visibility into every expense and decision becomes structurally impossible. At that stage, the informal financial management practices that worked when the founder could see everything directly begin producing financial blind spots simply because the organization has grown beyond the scope of personal oversight. Building reporting infrastructure before that inflection point produces the financial visibility that protects the growth period. Building it after means addressing blind spots that have already been compounding while the structure was absent.